What Should Seniors Know About Filing Taxes in Retirement?

Table of Contents

As retirement unfolds, it’s important to understand how taxes apply to your new financial landscape. From retirement income sources to deductions and tax strategies, managing your taxes effectively can protect your savings and ensure financial peace of mind.

This guide highlights key tax considerations for retirees to help you navigate this often-overlooked aspect of retirement planning.

Key Takeaways

- Different retirement income sources have specific tax rules, and understanding them helps you reduce your tax burden.

- Using tax deductions, credits, and strategies like Roth withdrawals can lower taxable income and protect savings.

- Avoiding mistakes like missing RMD deadlines or underestimating Medicare costs helps prevent penalties and surprise expenses.

- Working with a tax professional ensures better planning for withdrawals, RMDs, and evolving tax regulations.

Retirement Income and Its Tax Implications

Retirement income comes from multiple sources, each with specific tax rules. Knowing how they interact can help minimize your taxable income and overall tax liability.

Here’s a breakdown of how common income sources are taxed:

Social Security Benefits

Social Security benefits are often a key component of retirement income. Depending on your combined income, up to 85% of your Social Security income may be taxable.

This taxation applies if your income exceeds specific thresholds set in the IRS Tax Guide based on your filing status.

Distributions from Retirement Accounts

When withdrawing money from your retirement accounts, how those distributions are taxed depends on the type of account.

Here’s what you need to know:

- Traditional IRA and 401(k): Withdrawals are taxed as ordinary income because these accounts are funded with pre-tax contributions.

- Roth IRA and Roth 401(k): Qualified withdrawals are tax-free, which can reduce your overall tax burden.

- Annuity Income: Depending on how the annuity was purchased, payments might be fully taxable or partially tax-free.

Investment Income and Capital Gains

Income from investments, such as dividends and interest, contributes to your taxable income. Long-term capital gains enjoy lower tax rates than ordinary income, whereas short-term gains are taxed at your regular rate.

Monitoring your portfolio can help you optimize tax efficiency.

Tax-Free and Tax-Exempt Income

Income from municipal bonds is typically tax-exempt at the federal level and sometimes at the state level.

Additionally, qualified distributions from Roth accounts remain tax-free if you meet eligibility criteria.

Pension Income

Pension payments are usually taxable with ordinary income tax rates. If you contributed after-tax dollars, a portion of your pension might be tax-free.

Retirement Tax Deductions and Credits

Deductions and credits tailored for retirees can help reduce your taxable income and overall tax bill.

Higher Standard Deduction

Seniors aged 65 and older benefit from an increased standard deduction, which reduces taxable income.

Medical and Medicare-Related Deductions

Medical expenses, including premiums for Medicare and supplemental insurance, are deductible if they exceed 7.5% of your adjusted gross income. This can be a significant advantage for those with high healthcare costs.

Credits for the Elderly or Disabled

Low-income seniors may qualify for a tax credit directly reducing their federal tax liability. Eligibility depends on your filing status, income, and whether you receive nontaxable Social Security or other retirement benefits.

Charitable Contributions

Donations made through a Qualified Charitable Distribution (QCD) directly from your IRA can count toward your RMD while reducing your taxable income.

How to Manage Your Taxable Income in Retirement

Strategically managing withdrawals and other sources of income can help you lower your tax liability and optimize your finances.

These approaches can help you make the most of your retirement savings:

- Tax Bracket Management: Large withdrawals from pre-tax accounts can push you into a higher tax bracket. Spreading distributions over multiple tax years can help manage your tax bracket effectively.

- Timing of Withdrawals: Consider delaying Social Security benefits to increase future payments and reduce taxable income in the short term. For a more tax-efficient strategy, pair this with withdrawals from Roth accounts.

- After-Tax Savings Accounts: Using funds from after-tax accounts can help you meet income needs without increasing taxable income.

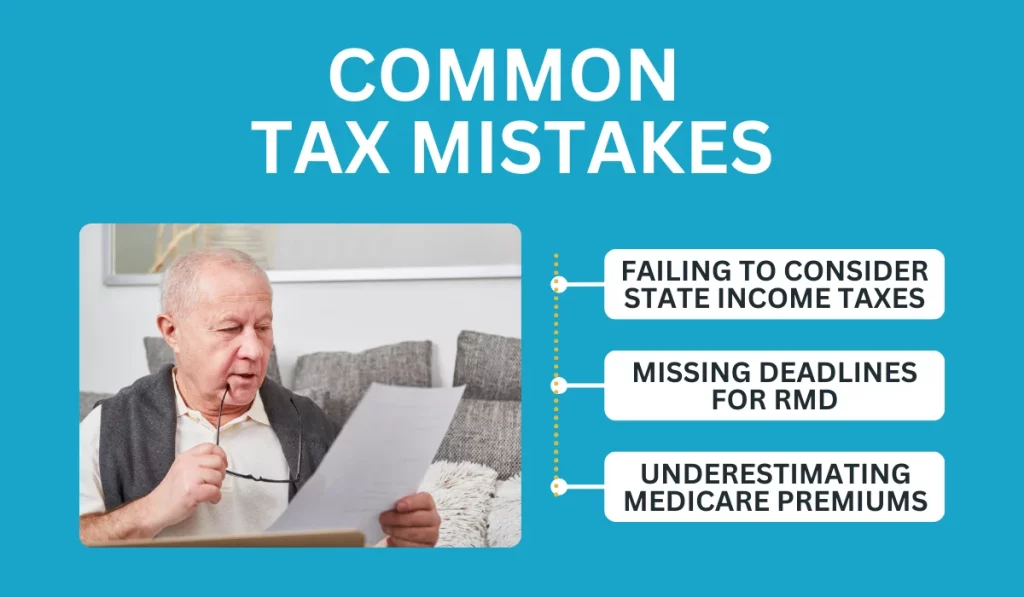

How to Avoid Common Tax Mistakes

Even minor oversights can lead to financial setbacks in retirement. Avoid these common mistakes to manage your tax obligations better:

- Failing to Consider State Income Taxes: Some states have favorable tax policies for retirees, exempting Social Security benefits or other retirement income. Research local taxes to understand your tax burden.

- Missing Deadlines for Required Minimum Distributions(RMD): To avoid penalties, RMDs must be taken from traditional IRAs and 401(k)s. For most retirees, this requirement starts at age 73.

- Underestimating Medicare Premiums: High taxable income can increase your Medicare Part B and Part D premiums through the Income-Related Monthly Adjustment Amount (IRMAA). Plan withdrawals carefully to avoid unexpected costs.

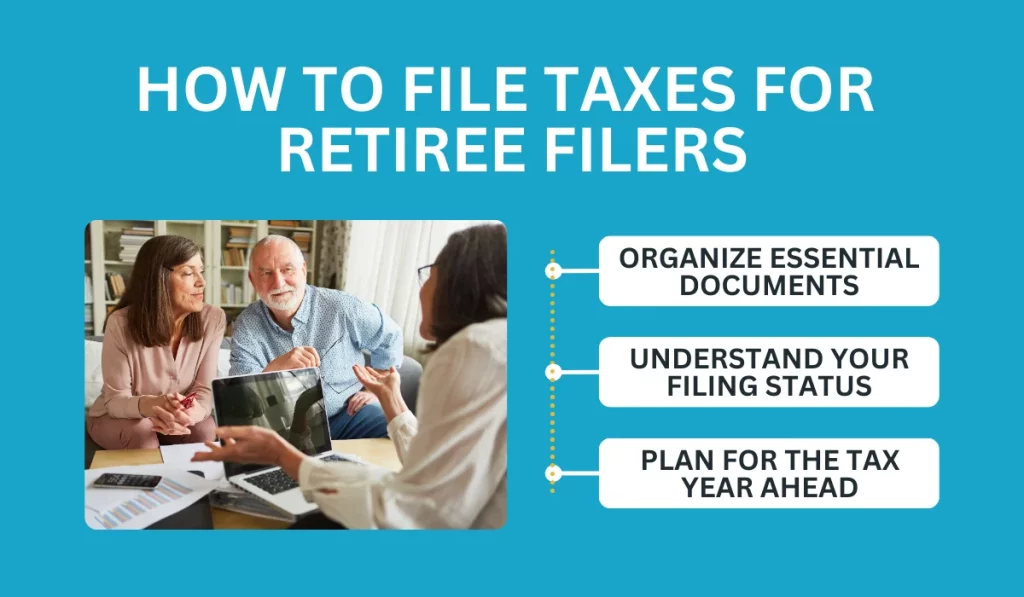

How to File Taxes for Retiree Filers

For simpler tax filing in retirement, follow these steps to stay organized and informed:

- Organize Essential Documents Gather all necessary forms, such as the 1099-R for retirement account distributions, the SSA-1099 for Social Security benefits, and the 1099-DIV for investment income.

- Understand Your Filing Status Your filing status affects your standard deduction and tax bracket. For example, “married filing jointly” generally offers more favorable tax treatment than “single” or “head of household.”

- Plan for the Tax Year Ahead Stay proactive by monitoring changes in tax laws, adjusting your withholdings, and making estimated tax payments if needed.

Partner with Professionals for Tax and Mobility Solutions in Retirement

Tax laws affecting retirees can be intricate, especially with multiple income sources and changing regulations. A qualified tax advisor can:

- Help calculate RMDs and plan distributions strategically.

- Review your tax bracket to optimize withdrawals and minimize taxes.

- Evaluate the tax implications of estate plans, including inheritance taxes for beneficiaries.

While managing taxes in retirement may seem overwhelming, professional guidance ensures compliance with tax rules and reduces the risk of costly mistakes.

At California Mobility, we encourage seniors to work closely with trusted tax professionals to navigate these complexities and protect their financial security. At the same time, we’re here to support your goal of staying safe and independent at home.

Contact us today to learn how we can help you stay confident and comfortable in your home.